Trump’s first month: What are the economic implications?

Leer en Español

Tariff threat distorts global trade and investment: So far, the U.S. president’s bark has been worse than his bite. Since taking office in January he has threatened to implement blanket tariffs on Canada, China and Mexico, impose reciprocal tariffs on the rest of the world, threatened to penalize foreign nations that impose digital services taxes on U.S. tech firms, and tax imports of steel and aluminum. Thus far, only the higher tariffs on China are in place. That said, the mere threat of greater U.S. trade restrictions has led companies to front-load goods shipments, boosting overseas exports data. At the same time, threatened tariffs are likely hampering overseas investment, while encouraging some U.S. firms to double down on domestic production: In recent days, Apple announced it would invest over USD 500 billion in the U.S. over the next four years, while drugmaker Eli Lilly unveiled a USD 27 billion investment in new manufacturing facilities.

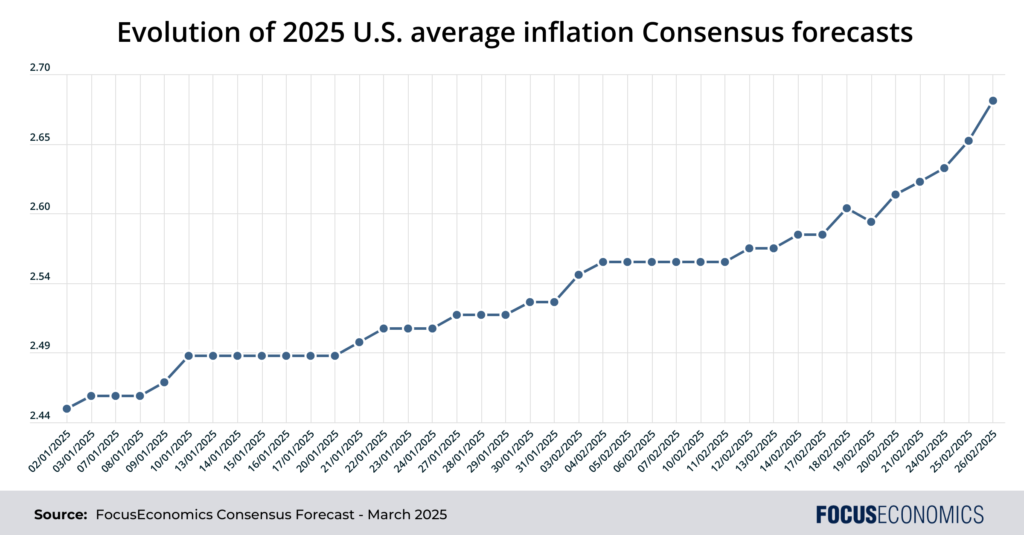

Inflation forecasts have risen: Our panelists have hiked their 2025 U.S. inflation forecasts by 0.3 percentage points since last December; U.S. inflation is now expected to be the highest in the G7 this year. Even though most of Trump’s tariff threats are still just that, our panelists expect his administration to follow through on at least some of them later this year, raising the average weighted U.S. tariff. The government’s intention to crack down on immigration is likely another factor behind the upward revisions. Higher inflation forecasts have fed through to hikes to panelists’ interest rate forecasts; several of our analysts now see the Fed on hold in 2025. World inflation forecasts are currently up by a milder 0.1 percentage points, though this figure would likely rise in the event of retaliatory tariffs by other nations.

Public spending cuts currently minuscule, but could increase: For all the furor surrounding DOGE—the Elon-Musk-led committee tasked with slashing government spending, cuts to date have been small. The committee’s own estimates—likely substantially overinflated—allege that savings worth USD 65 billion have been found. If true, that would amount to close to 1% of the Federal budget. The Federal budget is itself only part of total government spending, which also includes a sizable contribution from the states. Moreover, the lower house of congress recently passed a bill calling for USD 2 trillion spending cuts over the next decade. Even ignoring offsetting tax cuts in the bill, these spending cuts would still leave the country with a large fiscal deficit going forward—the deficit in 2024 alone was close to USD 2 trillion.

Institutional damage: A longer-term—and harder to calculate—risk is to the proper functioning of U.S. institutions, which have been a key pillar underpinning the economy’s immense wealth generation over the past century. The new U.S government’s moves to pack the judiciary with loyalists, rein in independent agencies and reduce the size of the federal workforce could in time reduce the effectiveness of government policy, while any attempt to bring the Federal Reserve under presidential control could cause financial instability and inflation to spike.

Insight from our analysts:

On tariffs, EIU analysts commented:

“Our baseline assumption is that the average weighted tariff on Chinese imports will rise by 20 percentage points to 30% by 2026. We also expect a more modest but still significant rise in tariffs on Mexico and Canada of up to 5 percentage points (from the current essentially zero level), and potentially on the EU later in 2025. The recent reintroduction of industrial metals tariffs is likely to stand, although some case-by-case exemptions will probably flow from negotiations over trade and other issues, including immigration and security.”

On inflation, Nomura analysts said:

“There is some sign of tariffs starting to affect some other inflation metrics. New York Fed’s 3-yr inflation expectations, which historically tended to move in tandem with gasoline price expectations, rose in recent months despite expectations for lower gasoline prices. As concerns over tariffs grow, we could also see a further pick-up in the New York Fed’s long-term inflation expectations.”

Our latest analysis

- Japan’s economy performed better than expected in Q4.

- Israel’s economy slowed in the fourth quarter.

The post Trump’s first month: What are the economic implications? appeared first on FocusEconomics.

Leave a Comment