Our Consensus Forecast for the U.S. fiscal balance and public debt

Leer en Español

In our latest special PDF report, we examine our Consensus Forecasts for the U.S. fiscal balance and public debt in light of a recent raft of policy changes by the Trump administration. Below are some key takeaways from that report.

Debt on the rise: U.S. public debt has climbed by about 30 percentage points as a share of GDP over the past 15 years, rising from just over 90% in 2010 to more than 120% in 2024. This shift has taken U.S. debt relative to GDP from well below the G7 average to above it. The increase is mainly due to a persistently high fiscal deficit averaging over 6% annually. Debt levels would be even higher if not for strong real GDP growth—the fastest in the G7—and recent high inflation reducing the real value of debt. The deficit reflects rising entitlement costs, political resistance to tax hikes, and major tax cuts under the first Trump administration.

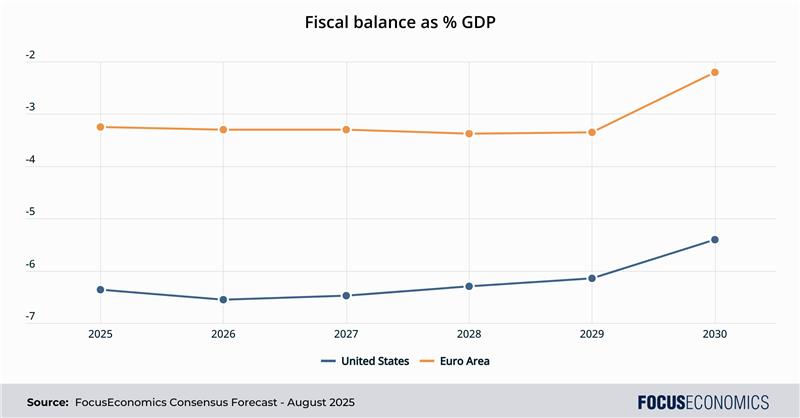

Fiscal metrics to remain concerning going forward: Our Consensus Forecasts suggest that the U.S. fiscal deficit will average over 6% of GDP through 2030—the highest rate among major advanced economies—driven by rising defense, border and pension spending, with little political will for offsetting tax hikes. Despite this, the public-debt-to-GDP ratio is expected to stay near 120%, as strong real economic growth and persistently above-target inflation help offset the impact of annual debt increases of around USD 2 trillion.

Is the U.S. fiscal position sustainable?: The U.S. is expected to meet its debt obligations under current conditions, with the public-debt-to-GDP ratio remaining relatively stable and below that of Italy and Japan; the dollar’s reserve currency status continues to support strong demand for U.S. debt. Key risks include a potential failure by Congress to raise the debt ceiling—though historically this has always been resolved—and the erosion of institutional integrity—such as threats to judicial or central bank independence—undermining investor confidence and complicating deficit financing.

Insight from our analysts:

EIU analysts commented:

“Government income from tariffs will rise, but not by enough to counterbalance the revenue foregone through tax cuts. Consistent with our tariff forecast, we also assume a 15% WATR over the medium term. […] Although the US is capable of meeting its debt obligations, political tensions remain a cause for concern. The debt limit was lifted by the recently passed budget bill, avoiding the previously looming deadline to raise the cap and extending the US’s ability to borrow into 2028. Beyond 2028, continued polarisation in Congress will keep the threat of a default alive, although this is not our baseline forecast.”

ING analysts said:

“US deficits will remain wide […], especially when we consider the continuous 0.1-0.2pp GDP increase in demography-related spending and how that will feed into the US’s fiscal position. Moreover, the combination of [tariffs and DOGE spending cuts] is likely to be detrimental to economic growth in the near term, which runs the risk of official deficit and debt projections being too optimistic.”

Our latest analysis:

- The Fed stayed on hold in July amid tariff uncertainty.

- Mexico’s economy was unexpectedly strong in Q2.

The post Our Consensus Forecast for the U.S. fiscal balance and public debt appeared first on FocusEconomics.

Leave a Comment