Which Countries Have the Highest Public Debt Levels in the World?

Leer en español

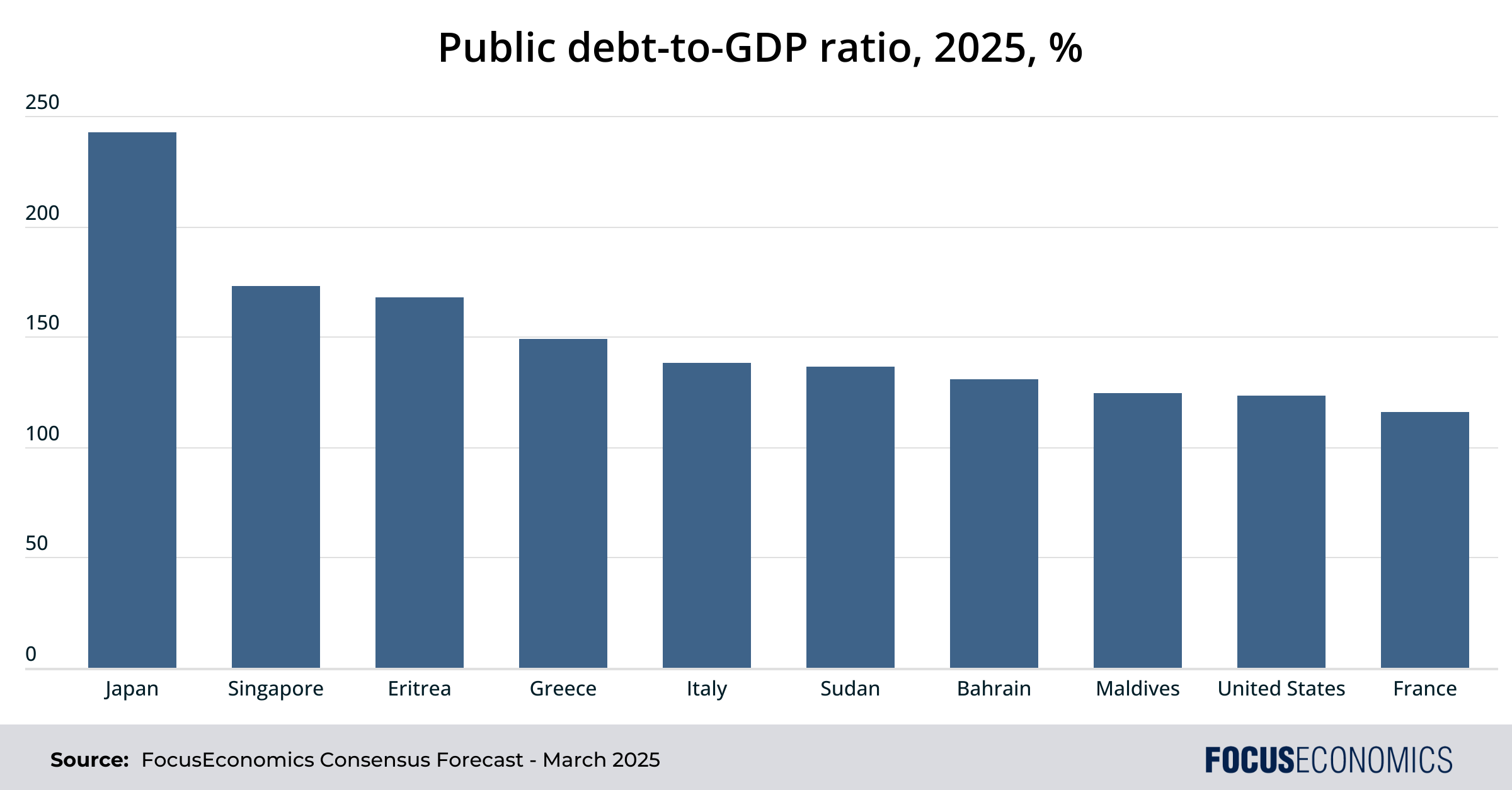

Ranking of Countries by Public Debt Level

Public debt refers to the total financial obligations of a country’s government, including bonds and other securities. This debt can be sourced both domestically and internationally. Issuing public debt is a crucial tool that governments use to fund public expenditures and address budget shortfalls. To facilitate comparison between countries and assess a country’s effective debt burden, public debt is typically measured as a percentage of Gross Domestic Product (GDP). Below is a list of the top 10 countries that will have the highest public debt-to-GDP ratio in 2025, according to our panel of analysts.

What is the Country with the Highest Public Debt Level?

Japan is the country expected to have the world’s highest public debt-to-GDP ratio this year, 242%. This high debt burden is relatively recent: In 1990, the ratio was only around 50% of GDP. However, that figure has subsequently surged due to aggressive government spending aimed at reviving an economy stalled by the collapse of the asset-price bubble in the early 1990s. Successive administrations have launched expansive stimulus packages, including substantial infrastructure projects and extensive social welfare spending, to combat persistent deflation and low growth. Moreover, a rapidly aging population has amplified expenditures on healthcare and pensions, significantly adding to the debt burden. Interestingly, despite these immense obligations, Japan’s debt does not tend to disrupt its economy, as it is largely held by domestic investors and institutions, including the Bank of Japan, which in turn maintains low borrowing costs. Nevertheless, Japan faces long-term vulnerabilities from rising debt-servicing costs if interest rates increase; our panelists are indeed forecasting higher interest rates going forward. This could crowd out crucial investment in growth areas. Thus, while manageable in the short term, Japan’s public debt still poses long-term risks to economic stability.

Remaining Top 10 Most-Indebted Countries

Country 2: Singapore

Our Consensus forecast is for Singapore’s public debt to be 173% of GDP in 2025. However, this high figure is due to intentional government policy rather than economic distress. Singapore strategically issues domestic debt to foster financial market development, particularly to support the mandatory savings scheme (Central Provident Fund). Unlike most heavily indebted countries, Singapore consistently maintains budget surpluses and substantial foreign reserves, resulting in virtually no actual fiscal strain; the government does not use debt financing to cover budget deficits or operating expenses. Consequently, unlike traditional high-debt scenarios elsewhere, Singapore’s elevated public debt is neither problematic nor economically limiting; instead, it reflects the country’s prudent and strategic financial management.

Country 3: Eritrea

Eritrea’s public debt—estimated by our panelists to clock in at 210% of GDP in 2025—is so high partly due to prolonged military conflicts, including war with Ethiopia in 1998–2000 and the more recent Tigray conflict. Continued mandatory military service has also diverted labor and investment from productive sectors, severely limiting economic diversification. Additionally, Eritrea’s restrictive economic policies, such as tight state control over industries and limited private sector engagement, have undermined growth, constrained revenue generation and increased reliance on external borrowing from China and other bilateral creditors. Eritrea’s international isolation, intensified by past sanctions and diplomatic tensions, further hamper opportunities for debt relief or debt restructuring. Consequently, the country’s high debt level is a critical economic constraint, stalling long-term development, exacerbating poverty and perpetuating the nation’s dependency on external financial assistance. Partly for this reason, Eritrea is and will continue to be among the world’s poorest nations in per capita terms.

Country 4: Greece

Greece’s public debt became so elevated primarily because of decades of unchecked government spending, widespread tax evasion and structural inefficiencies in the economy. These weaknesses were dramatically exposed during the 2008 global financial crisis, plunging Greece into severe recession and forcing multiple international bailouts accompanied by stringent austerity measures. The resulting debt crisis severely impinged Greece’s economic performance, causing a prolonged period of recession, high unemployment and declining standards of living in the early to mid-2010s. Since the pandemic, Greece’s public debt burden has tumbled by over 50 percentage points amid strong economic growth and prudent fiscal policy, but is still expected to be among the highest in the world in 2025 at 149% of GDP. Encouragingly, this sharp downward trend is expected to persist in the coming years, with the country’s public debt-to-GDP ratio forecast to converge towards the Euro area average over the next decade. However, the debt burden will continue to require careful fiscal management and will constrain Greece’s ability to implement expansionary fiscal policies.

Country 5: Italy

Italy’s elevated public debt results from decades of sluggish economic growth, structural inefficiencies and consistently high government spending on pensions and social welfare programs. During the European debt crisis of the 2010s, Italy was one of the countries most at risk—one of the so-called PIGS—despite never requiring a formal bailout. The combination of weak GDP growth and elevated spending demands will keep the budget deep in the red and Italy’s public debt high in the coming years; our current Consensus forecast is for a public debt-to-GDP ratio of 138% in 2025. Italy is arguably the euro area’s weakest fiscal link, given the country’s elevated public debt forecasts combined with the economy’s sheer size.

Country 6: Sudan

Sudan’s public debt is forecast to be 128% of GDP in 2025. This figure is more than double the average for emerging markets, and results from prolonged internal conflicts, economic mismanagement, international sanctions and the devastating economic impact of South Sudan’s secession in 2011, which drastically reduced oil revenues. These factors forced Sudan to rely heavily on external borrowing to finance budget deficits, fueling chronic economic instability. The debt burden significantly limits fiscal space, in turn restricting investment in critical infrastructure, public services and economic diversification, thus hindering growth and development. While recent international engagement and debt relief initiatives have begun addressing Sudan’s debt challenges, the country remains highly vulnerable. Persistent political instability—including the devastating civil war that has played out since 2023—and limited economic reforms continue to make it difficult for the government to manage its debt burden.

Country 7: Bahrain

Bahrain’s public debt-to-GDP ratio roughly tripled between 2012 and 2023, with the surge attributed to several factors. The 2014–2016 collapse in global oil prices reduced hydrocarbon revenues, exacerbating fiscal deficits as a result. Rising military and security spending in response to regional instability further strained public finances, while initiatives to diversify the economy necessitated substantial public investments. In 2018, Bahrain received a USD 10 billion financial support package from neighboring Gulf countries, conditional upon implementing fiscal reforms, including the introduction of a value-added tax (VAT). Despite these measures, Bahrain’s public debt remains a concern and is expected to rise further as a share of GDP in the coming years; for 2025, our panelists pencil in a reading of 131% of GDP. The government’s aversion to substantially raising taxes, coupled with rigid social spending demands in order to ensure social stability, will stoke public debt going forward.

Country 8: The Maldives

The Maldives’ public debt has escalated significantly in recent years. This surge is partly due to extensive borrowing for ambitious infrastructure projects, such as the China-Maldives Friendship Bridge and the expansion of Velana International Airport. Additionally, the Covid-19 pandemic severely impacted the tourism-dependent economy, which contracted by a third in 2020, requiring increased government expenditure to mitigate the downturn; in the same year, the fiscal deficit swelled to more than a fifth of GDP. The country will remain at risk of debt distress going forward, with heightened debt servicing costs projected to average around USD 600–700 million in 2025–26. That said, strong tourism revenue and foreign financial support—particularly from India, which late last year announced a bailout package for the archipelago—should aid financial stability. Our Consensus is for the public debt-to-GDP ratio to be 125% of GDP this year.

Country 9: The United States

The United States’ public debt has sharply increased so far this century due to frequent tax cuts, rising entitlement spending and policy responses to the Global Financial Crisis and the Covid-19 pandemic. Higher entitlement spending is linked to the aging population and rising healthcare costs associated with programs like Medicare and Medicaid. The country’s debt burden is currently manageable, as the dollar’s status as the global reserve currency keeps borrowing costs low and ensures strong market demand for U.S. Treasury bills. However, the need for Congress to periodically raise the debt ceiling to allow more borrowing creates uncertainty; without the periodic re-rating of the ceiling, the federal government would be forced to cut back spending or default on debt. The new government under Donald Trump is attempting to hack away at public spending through the new Department of Government Efficiency. For all the media hype surrounding the department, cuts to date are likely small and several cost-saving measures are already being challenged in the courts. For now, our panelists continue to forecast the U.S. to run the largest deficit in the G7 in the coming years, and for public debt to remain on an upward trend as a share of GDP, reaching 124% of GDP this year.

Country 10: France

Since 1975, France has consistently run budget deficits, leading to a steady accumulation of public debt. Sluggish economic growth, a generous welfare state and the public’s aversion to any form of fiscal consolidation—often manifested in violent protests such as the Yellow Vest movement—have all contributed to persistent fiscal shortfalls. The 2008 global financial crisis and the Covid-19 pandemic further exacerbated this trend, with the latter prompting extensive government spending to support the economy. The country currently has one of the largest fiscal deficits in the EU; in 2024, France was reprimanded for flouting the bloc’s rule mandating a deficit of less than 3.0% of GDP. The new government of Francois Bayrou has pledged mild budget consolidation in the coming years, though this won’t be enough to put a dent in France’s public debt pile. Our Consensus is for the public debt-to-GDP ratio to be 116% in 2025 and to rise towards 120% by the end of the decade, posing risks to financial stability.

Originally published in July 2023, updated in March 2025

The post Which Countries Have the Highest Public Debt Levels in the World? appeared first on FocusEconomics.

Leave a Comment