China’s Economic Outlook for 2025 and Beyond

Leer en Español

China’s GDP Growth Target for 2025

Official Growth Target and Economic Policy Goals

In March 2025, the central government announced that China’s GDP growth target would be “around 5%” for the year, reaffirming its focus on stability in an increasingly volatile global economic environment. This target, unveiled at the annual National People’s Congress (NPC), signals a continuation of the country’s moderate growth trajectory following the pandemic-related disruptions of the early 2020s.

Unlike the double-digit growth rates of previous decades, the around-5% figure is not intended to dazzle investors or signal explosive economic resurgence. Rather, the goal is to foster sustainable, high-quality development while simultaneously mitigating financial risks, navigating demographic headwinds, and addressing weakening global demand.

That said, the target is still above market expectations of China’s 2025 growth rate, signaling that this year will see further stimulus measures and that the authorities are confident in the economy in the face of higher U.S. tariffs; Trump jacked up tariffs on China by 20% soon after taking office, and is set to raise tariffs further from 9 April as part of his “reciprocal tariff” plan.

The government’s approach, as outlined in Premier Li Qiang’s work report, emphasizes “steady progress” and the need for policy continuity. Fiscal and monetary levers will be used cautiously but deliberately: The 2025 budget includes a fiscal deficit ratio of 4.0% of GDP, up from a 3.0% target in 2024, suggesting a willingness to support growth so long as it doesn’t trigger inflation or exacerbate local government debt concerns. Special treasury bonds and infrastructure investment are expected to remain key tools for economic management, especially in sectors that promote green development, digital transformation and regional revitalization. There are also likely to be extra steps to shore up domestic consumption in the face of rising threats to the export sector—chiefly U.S. tariffs.

Furthermore, the growth target is framed by China’s broader strategic vision—transitioning from quantity to quality in economic output. The emphasis is on technological innovation, domestic consumption and supply-side upgrades, rather than replicating the old model of real estate-driven and export-led growth. In this context, the around-5% target is more than just a number; it is a policy compass for navigating a post-Covid-19, increasingly fragmented global economy.

On the government’s general policy direction, DBS analysts said:

“Advancing ‘new quality productive forces’ and technological innovation, particularly in artificial intelligence, remains central to China’s strategy. The government aims to foster ‘industries of the future’, including biomanufacturing, quantum technology, embodied AI and 6G by exploring new models for national laboratories and empowering young scientists and engineers with ‘important responsibilities’ and robust support. State-owned enterprises are mandated to prioritize AI development in the 15th Five-Year Plan, while parallel efforts to accelerate the Private Economy Promotion Law seek to dismantle barriers for private firms. These steps, alongside President Xi’s recent symposium with business leaders, signal a renewed pro-business stance and encourage greater private sector investment in innovation.”

Key Factors Influencing the 2025 Growth Target Decision

Several critical factors underpin China’s decision to set its 2025 growth target at around 5%:

- Post-Pandemic Recovery Trajectory

Although China rebounded relatively quickly from Covid-19 compared to many advanced economies, the recovery has been uneven. While industriarl production has been robust, consumer confidence remains subdued, youth unemployment lingers above 14%, and the property market—once a core engine of growth—continues to undergo a painful correction. The around-5% target, which is below pre-pandemic targets, thus reflects post-pandemic scarring and structural weaknesses in the economy. - Geopolitical and Trade Headwinds

Tensions with the United States and its allies have escalated, particularly in trade, technology and investment. Tariffs on Chinese goods plus tech restrictions on Chinese firms have reduced the room for export-led growth. In this context, the government’s growth target accommodates reduced external demand and an ongoing pivot toward self-reliance. - Demographic Pressures

China is now aging faster than any major economy. In 2023, the country’s population shrank for the second consecutive year, and the fertility rate remains well below replacement level. A shrinking labor force and rising dependency ratio are expected to drag on potential growth for years. Setting an around-5% target acknowledges these limitations. - Structural Debt and Financial Risks

Years of aggressive credit expansion—particularly by local governments and state-owned enterprises—have created a complex web of financial vulnerabilities. The central government is now attempting to deleverage without derailing growth, and the around-5% target is intended to give breathing room for debt restructuring and prudent risk management while maintaining macroeconomic stability.

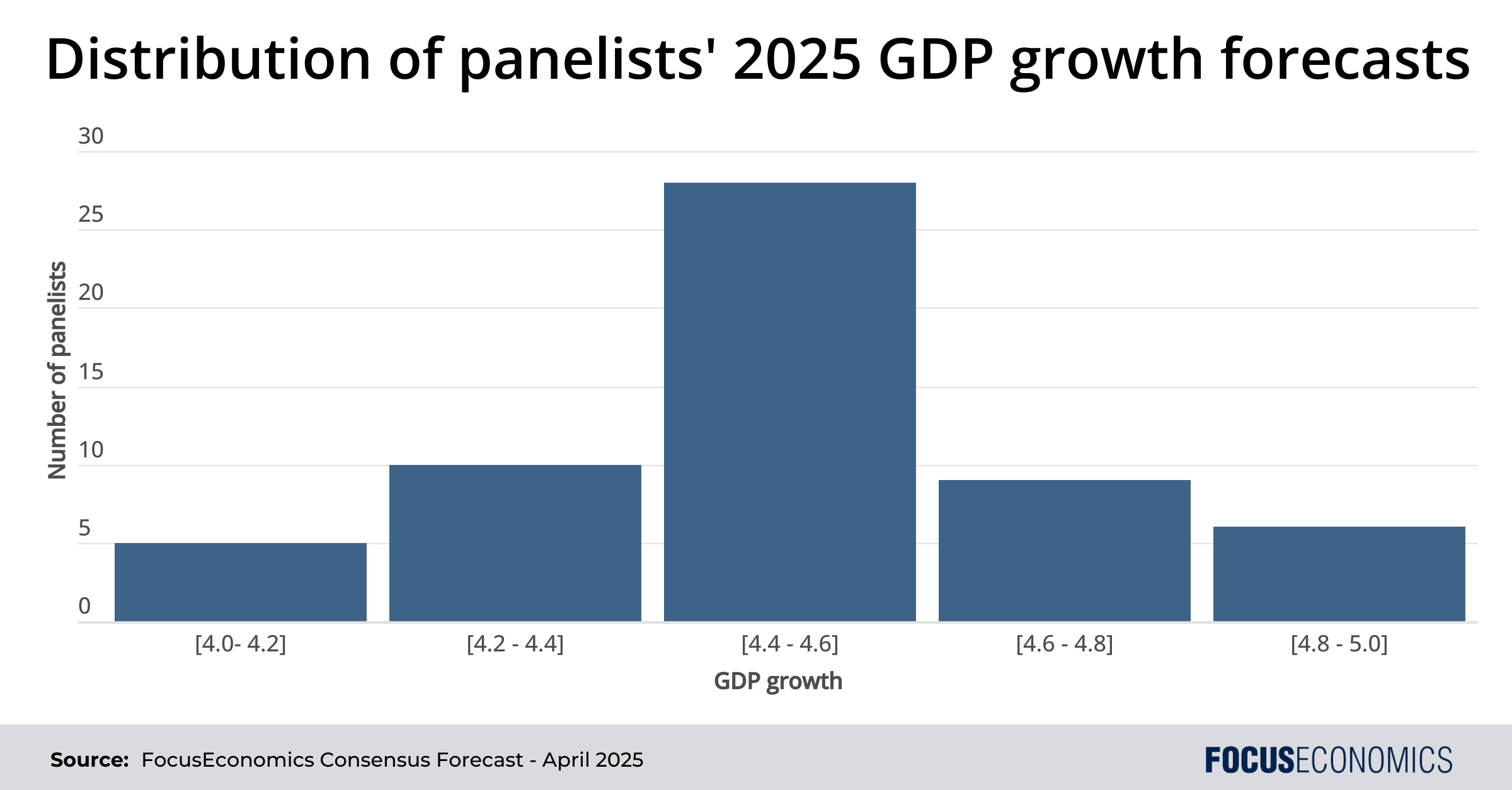

Economic Growth Projections: Consensus Projections vs. Official Targets

Our panelists don’t expect the growth target to be met, with our Consensus forecasts currently for a 4.5% annual rise in GDP this year. If confirmed, this would be the weakest reading in decades when excluding the periods affected by the Covid-19 pandemic. Panelists’ downbeat assessment is based on the multiple headwinds coming China’s way.

The first and foremost is tariffs. If Trump follows through on “reciprocal” tariffs, average U.S. tariffs on Chinese imports will rise to over 70%. This would likely be a level high enough to make selling to the U.S. unprofitable for many Chinese firms, while those that remain will lose market share. Then there’s the impact on the rest of the world: Trump plans to jack up tariffs on all imports, which will hit global demand and thus appetite for Chinese goods.

Domestic challenges are widespread too, in the form of a still-sluggish property sector, cash-strapped local governments and overcapacity in the alternative energy sector. Regarding the former, home prices, real estate investment and construction activity all fell in January–February in annual terms.

Then is China’s current trade-in program for goods: The program has caused consumers to front-load purchases, providing a temporary boost to retail sales. But this could lead to a corresponding drop in consumer demand later in the year.

Commenting on China’s growth target, Nomura analysts said:

“We agree with Li’s comment that ‘achieving this year’s targets won’t be easy’, and we maintain our GDP growth forecast for this year at 4.5% despite the “around 5.0%” government target. We expect growth to drop towards 4.0% at year-end, and Beijing might once again be compelled to ramp up policy support in H2. Despite many calls to significantly raise pension and medical care subsidies to less-privileged groups – especially the 173mn elderly who do not receive formal retirement payments (predominantly farmers) – the steps Beijing took appear somewhat small. Beijing did double the consumer trade-in program to RMB300bn this year, but we expect a rapidly tapering impact after Q1.”

The economy will have some things going in its favor though. Apart from a looser fiscal stance, our panelists expect further monetary policy easing later this year in the form of cuts to interest rates. The rapid infusion of AI through the economy could give productivity a boost; recent surveys point to a faster uptake of generative AI software in China than in the U.S. for instance. Spending on AI will surge. And optimism over the sector in the wake of DeepSeek’s breakthrough large language model has boosted Chinese stocks, which could aid investment and consumption in turn; the Hang Seng share index is up over 10% so far this year. Moreover, the government has recently signaled a warmer attitude toward the private sector after bashing major tech firms such as Alibaba in 2020–2022; notably, Alibaba’s founder Jack Ma attended a high-level meeting with Xi Jinping earlier this year. This warmer attitude could support private investment.

Regarding prices, our panelists expect inflation to average 0.6% in 2025, well below the 2.0% target. This will be a reflection of sluggish GDP growth, fierce competition plus overcapacity in key sectors, stabilizing pork prices and softer currency depreciation relative to last year. One of the few upside risks comes from Chinese retaliation to U.S. tariffs, which could see import prices rise.

On prices, EIU analysts said:

“Consumer price inflation will remain very weak, even as it begins to trend upwards in 2025 […]. Aware of the deflationary pressures gripping the country, policymakers will attempt to reflate the economy via public spending and monetary easing; however, the impact will be limited. Housing costs, an important component of the inflation basket, will continue to act as a drag (albeit diminishing). Overcapacity and higher trade barriers for exports will weigh on producer prices, while weak household and business confidence will encourage value-for-money purchases, putting further pressure on core inflation. Sources of inflation will primarily include government-stimulated domestic demand, which will help to support domestic commodity prices.”

Uncertainties and Risks for China’s 2025 GDP Target

Clarity over the outlook for this year is lacking, with three key factors at play:

- U.S. tariffs

Though the U.S. has already implemented tariffs on China, it’s not clear for how long such tariffs will remain in place, or whether a deal could be reached between the two superpowers to improve market access. Trump’s trade policy in his early months in office has been volatile, with constant flip-flopping on the tariffs imposed on Canada and Mexico, suggesting hope for some roll-back of tariffs on China in the future. - Domestic stimulus measures

In March, the government talked up the importance of “vigorously boosting consumption”. The effectiveness of these measures will be key to watch, as private spending is a large untapped well of potential economic growth given how much less China’s citizens spend relative to those in many other nations. - The impact of AI

Chinese private and state firms have avidly adopted AI recently, particularly since start-up DeepSeek announced a world-class model earlier this year; dozens of local governments in China have reportedly already integrated DeepSeek’s model into their operations. A combination of a tech-friendly populace and weak rules over copyright and data privacy could allow AI to permeate more quickly in China than in most other countries, posing an upside risk to productivity and GDP growth.

China’s Economic Growth Outlook

Short-Term vs. Long-Term Projections

Beyond 2025, China’s economic outlook is muted: our Consensus is for China’s GDP growth to slide to below 4% by 2028, and to be only slightly above 3% in a decade’s time. This is a reflection of increasingly dire demographics—the population will be falling by two million a year by the end of this decade—as well as the fallout from U.S. trade restrictions and a natural slowdown in the rate of growth as the country becomes wealthier and approaches the technological frontier.

On trade, export restrictions with the West—especially the United States—will cap the Chinese economy. While Chinese firms will continue to make inroads in southeast Asia, Africa and Latin America, even there firms may face increasing entry barriers, as many governments grow concerned about an influx of cheap Chinese goods undercutting local companies. For instance, last year Indonesia’s government floated high tariffs on Chinese imports including textiles and ceramics, while Thai firms have called for similar measures in their country. In short, the contribution of China’s exports to overall GDP growth will be constrained going forward.

Factors like strong government investment in R&D and high-end manufacturing, particularly in “new quality productive forces”—a term that encapsulates AI, clean energy, robotics and biotechnology—won’t be enough to stem the growth slide. Meanwhile, inflation is seen averaging between one and two percent, while the fiscal deficit will remain broad as the government continues to stimulate the economy to ward off deflation.

On the likely boost from AI, Goldman Sachs’ analysts said:

“The release of DeepSeek’s model, which may have been developed at a lower cost than other leading models, suggests a faster adoption rate and greater economic upside for China than previously anticipated […]. Faster adoption of generative AI in China could translate into lower labor costs and higher productivity as more tasks are automated. Goldman Sachs Research now estimates that generative AI will start raising potential growth in China by 2026 and provide a 0.2-0.3 percentage point boost to China’s GDP by 2030, up from 0.1 percentage point previously.”

On long-term inflation, EIU analysts said:

“Inflation will pick up later in our forecast period but remain significantly below the government’s (largely symbolic) target of 3%, averaging 1.1% in 2026-29. The supply-demand imbalance will persist, maintaining some overcapacity strains. Limited improvements in social welfare will constrain inflation through lower private consumption, but a labour shortage will emerge over time—probably beyond our forecast period—putting a floor under wage growth and inflation in the services sector.”

Domestic Economic Reforms and Their Potential Effects on GDP

China is crying out for structural reform to boost sagging total factory productivity growth; such reforms would likely yield higher GDP growth than our panelists currently project. However, the authorities have not so far shown an appetite for radical reform, with an emphasis rather on incremental change that preserves economic and social stability above all else. A lack of reforms going forward raises the risk of a prolonged period of secular stagnation, akin to the post-boom phase experienced by Japan from the 1990s to the present day.

There are plenty of areas for action, including:

- Household income and social safety nets

Private consumption is still around 20 percentage points of GDP lower in China than in developed economies. The major drag on consumption is high household saving rates, driven by inadequate pensions, healthcare coverage and education costs. Expanding social welfare programs—such as unemployment benefits and universal health insurance—could unlock substantial consumer spending, directly supporting GDP growth. - Urbanization and labor mobility

China has eased hukou (household registration) restrictions in second- and third-tier cities in recent years, allowing more rural migrants to settle in urban areas and access public services. Further liberalization of the system, or the scrapping of hukou altogether, would boost urban consumption and facilitate a more efficient labor market. - Boosting the private sector

Private firms—which are on average far more productive than their state counterparts—have lost their sheen over the last decade as the government has prioritized economic and social stability above all else. Leveling the playing field between private and state firms plus reducing the influence of the state in the allocation of resources would likely give productivity a welcome lift.

Originally published in January 2024, updated in April 2025

The post China’s Economic Outlook for 2025 and Beyond appeared first on FocusEconomics.

Leave a Comment